Opus 24: Investing Adventures in Uzbekistan

The capital markets of the silk road

Introduction

I recently visited Kazakhstan and Uzbekistan as part of the research trips I am conducting for my Imperium work. The Uzbek portion of the trip was organized by a local fund that manages a domestic public equities fund which was set up in 2021 on the back of the reforms Uzbekistan’s president has been pushing to open up the country. We were fortunate to visit a number of companies during our trip, many of which are publically traded on the domestic market.

Uzbekistan is becoming more popular for both regional and global tourism, given its historical significance as part of the Silk Road and thousands of years of recorded history. I highly recommend everyone visit the country, experience its warm hospitality, enjoy its wonderful food, and witness its growth as one of the fastest-growing countries in the world today.

The below post will follow the format of my other “Investing Adventures” posts (available here, here, and here) where I share thoughts on the country’s economy and capital market before highlighting a few specific businesses. Unlike my other trips, I was actually able to meet with some of these businesses, which provided a more intimate understanding of their operations, outlook, and investment case.

I am sure I have made mistakes throughout this post given much of the information requires translation from Russian or Uzbek and Google Translate and AI translation are imperfect tools. I have done my best to present things accurately, but please comment or reach out if you have any corrections to make!

A Brief Overview

Population - 36M, growing ~2.5% per annum with a total fertility rate of 3.17 which is one of the highest in the world outside of Africa. Only Afghanistan, Pakistan, and Iraq are higher outside of the African continent

GDP - $80B

GDP Growth - 5.3%, 35th highest in the world

GDP per capita PPP - $9,724

Size - 173,000 sq miles, similar to Sweden and Morocco

Inflation - ~12%

Biggest exports - Gold (30%), Cotton (8.3%), Gas (5.5%), Copper (3.5%)

Median age - 29

Uzbek Economy

For all intents and purposes, Uzbekistan was a closed country until 2017 when its authoritative leader died. Since then, the country’s new leadership has reformed most of the economy by opening up to foreign direct investment, foreign competition, currency devaluation, and regulatory changes to make the country a more business-friendly free market. The country has seen rapid growth since then with GDP growth remaining in the top decile globally.

Uzbekistan’s economy is fairly diversified, especially compared to its neighbors such as Kazakstan which is mostly reliant on gas and oil. Half of the economy is services with agriculture and industry making up the balance at 18% and 33% respectively.

In recent years, tourism has accelerated with people from around the world coming to see the historic cities of Samarkand, Kiva, and Bukhara. In 2023 the country welcomed 6.6 million tourists, a 2.5x increase compared to 2017. The government has done a great job highlighting the country’s historical importance and PR is continuing to pick up about Uzbekistan as a world class travel destination.

The Uzbek currency, the Som, loses ~6% a year against the USD. The country has gone through several devaluation exercises as the government looks to reform the economy and get rid of the currency black market. Central bank intervention has been minimal except in some cases of extreme currency volatility. The bank has generally accepted the constant devaluation as the country continues to lean on its exporting market to grow the economy. There is still a small currency black market in the country which you experience at the airport and other tourist hubs where people with wads of local currency go around offering slightly better rates than you can get from the ATM.

An interesting human capital data point that Uzbekistan can leverage is its massive student population that studies abroad each year. The country ranks 5th in the world (on an absolute basis) for number of students studying abroad each year. Many of these students are on government funded scholarships that require the students to return home. This well-educated base of students will fuel the continuing growth of the country.

Uzbek Reforms

One of the reasons I was interested in visiting Uzbekistan was its active reform programs that the government is leveraging to open up and liberalize its economy. Most of these reforms focus on decreasing the State’s economic role. This includes indirect subsidization and tariffs, as well as more direct involvement through state-owned enterprises and government-controlled markets like the banking sector.

While painful, the reforms are necessary and the government recognizes this. Recent activity has slowed after a few initial years of action, including regulatory reforms, privatization of some state-owned enterprises (SOEs,) and changes in energy tariffs. Many people argue that the “easy” things are done and now the government must reckon with the much harder tasks with many vested interests leading to political pushback.

In recent conversations, it seems that important things are happening behind the scenes on the SOE reform / privatization front with international funds coming in and assisting the government. These changes will lead to massive changes within the economy. The largest SOEs provide the government with nearly 35% of its annual budget. In aggregate, the SOEs produce $12B in annual income, more than 15% of the country’s GDP. There are clear interests throughout the government that wish for the status quo to remain, but it is encouraging to see the political will at the top wanting to force change.

Uzbekistan Stock Exchange

Uzbekistan’s stock exchange - formally known as “Republican Stock Exchange Tashkent” - was formed in 1994 after Uzbekistan’s independence from the USSR. The exchange is majority owned by the Government, and the Korean Stock Exchange owns 25% which they acquired in 2012 as part of a technology-sharing agreement.

The capital market is quite nascent. The exchange recorded ~$200M in 2023 trading volume with many securities not being traded at all. Unfortunately, the exchange saw a 80% decrease in H1 2024 compared to the same period of last year with only $35M in total volume - this is mostly explained by the abscenese of large M&A deals driving volume. In our meeting with the exchange, the CEO shared that the exchange is nearing the finalization of its connection to Euroclear and other global liquidity channels in order to make the market more accessible to international capital. This should help with some liquidity issues but the exchange needs the country’s best companies to list significant equity in order to see any real activity.

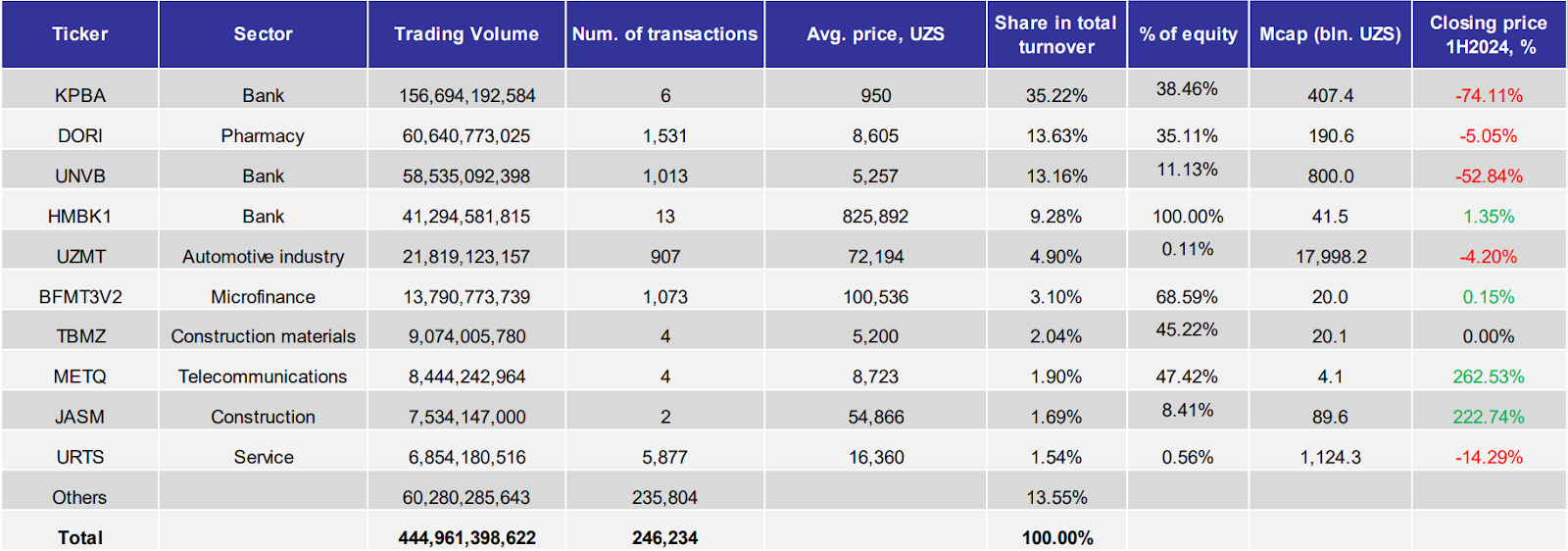

Share volatility is a problem in most emerging markets where bid and ask spreads are wide enough to drive a truck through them. This causes share prices to swing 50+% in just a number of days. Avesta, the leading investment bank and advisory group in Uzbekistan, published the 10 most liquid equities in H1 2024 below. Notice how even the most liquid names have swings of 200+% in just 6 months.

The exchange has 103 listings, most of which are equities. Interestingly, 8 out of the 10 largest companies by market capitalization on the Uzbek Stock Market are banks. The state-owned gas company and steel company are the only two exceptions.

Overall, the information on the exchange is quite difficult to understand and access, with most companies not reporting English financials, disclosures, or reports. Market data is unclear with no ability to do long look back periods of prices, financial information is not organized nor published in a regularly scheduled, chronological order and usability is quite poor.

One of the people on our tour set up a far more user-friendly website to interact with the market data and see financial information for all of the companies. Many companies have not shared results, board minutes, etc. for years. There is a general sentiment that the Uzbek capital market is not mature or large enough to be taken seriously yet. I think there are relatively simple things like proper disclosures, standard reporting schedules, English translation in reporting, and better information usability that could all assist in this mission to get the capital market ready for the global stage. The country has exciting, secular trends that will create a foundation for great companies to be built, but if governance, disclosures, and transparency cannot be done correctly much of this potential will be wasted.

Now, let’s dive into a few specific companies.

Uzbekistan Commodities Exchange, UZEX ($88M market cap)

The Uzbek Commodities Exchange (UZEX) is another state-owned exchange venue that listed a small portion of its equity on the domestic stock exchange. As the name suggests, the exchange is the central venue for all commodities trading in the country such as metals, agricultural products, commodities, and other random items - more on that below. The exchange acts as an anti-corruption mechanism, so all commodity procurement happens in the open and at market prices. The government - via UzSAMA, the state asset management company - owns 45% of the company, Trastbank owns 19%, and Presystem Universal LLC owns 18%. The remaining 18% is listed as “other minorities” with no further details.

When you dig into the non-state ownership a bit, you will find that Trastbank is the custodian bank for the exchange, and many related parties are involved. Karimova Maxira Shadibekovna is listed as a board member of both UZEX and Trastbank and is the only listed director or affiliate of “Presystem Universal LLC.” There is no published website or well-documented information on this entity beyond a mention in the Uzbek yellow pages that the company operates in the plastic paneling and metals industry, which I must assume means it is heavily involved in the exchange. The entity's only contact information is a mail.ru email address: presystem@mail.ru. The Stock Exchange awards UZEX with a 100% score on corporate governance which seems a bit strange when there are clear conflicts of interest at the board level between affiliated parties.

The exchange mostly focuses on commodities trading but also manages platforms for government procurement, logistical services (freight brokerage), non-standard items (furniture, hard assets, etc.) and the issuance of license plates and mobile phone numbers. The exchange is the Ministry of Transportation’s only outlet for people to purchase license plates. This leads to competitive bidding on custom plate numbers and auspicious numbers such as 777 or other lucky numbers. The most expensive license plate ever sold in Uzbekistan was $45,000, or roughly 5x the average annual income of an Uzbek citizen. This would be like an American citizen paying the DMV $185,000 for their lucky license plate number.

One of the strangest things about the exchange is a law requiring that it pays ~20% of all revenue, not profit, to the Ministries of Economic Development, Poverty Reduction, and Finance as a sort of tax on its financial trading activities. On the ~$35M in revenue the company booked in 2022, nearly $6M was directly sent to these Ministries. This bizarre claim on revenues is a good example of some of the leftover issues from the country’s history that weigh on its ability to attract foreign capital.

We visited the exchange’s office during our trip and had the opportunity to speak with management. It was a wonderful experience and allowed us to better understand the business’s operations, strategic goals, and outlook. However, any questions regarding the company’s ownership, disclosures, or the strange tax that the government has on its revenue were met with awkward frustration, and the management team would speak amongst themselves before providing an answer. Often, this answer was vague and diverted from the question. There seems to be tension between the company’s management and shareholders and what should be disclosed publicly. When asked if any of the management team owns shares in the company, they all laughed and said “No, that does not exist here.”

From 2018 to 2022, the company grew revenue by an average of 39% per annum in local currency. For the first time, the company’s revenue shrank in 2023, which management blamed on the energy crisis. The crisis led to many industrial factories shutting down for the winter, leading to less domestic commodity production. This same issue is shared by many industrial businesses in the country that could not run their plants for an extended period.

From 2018 to the peak in 2021, the company’s equity appreciated nearly 30x in value. Since the peak, the company has lost ~50% of its value in volatile trading. This is a great example of the whiplash-like volatility one can experience in thinly traded emerging markets where just $1,000 in bids can cause a company to jump on one trade. To give a sense, the average monthly volume for UZEX’s equity is ~$80,000 / month for the last two years. The exchange does not show order book depth, but it is safe to assume that a $10,000 order could move the price 25% at a moment’s notice.

The business pays out ~80-85% of its earnings each year in the form of dividends. As of the time of this writing, the shares are trading at a ~17.5% dividend yield, assuming the dividend policy and relative earnings power of the business maintain their H1 levels.

As Uzbekistan continues to develop, the commodities exchange should be a good proxy for the country’s growth given the sheer amount of industrial products needed for the construction and development happening in the country.

Uzmetkombinat, UZMK ($190M market cap)

One of the country’s most well-known companies is the State-owned steel company UzmekKombinat. The company is 54% owned by the Ministry of Economy, 38% by the Recovery and Development Fund of Uzbekistan, and 8% owned by “other legal and individual entities” with no further disclosure. As part of the ongoing reforms, the company floated ~5% of its share capital on the Tashkent Exchange in 2022.

Originally built in 1944 as a Soviet steel factory, the business was transformed into a joint stock company in 1994. Uzmetkombinat has a legal purchasing monopoly over the country’s domestic scrap metal, which it uses as the main input for the two main products: long beam products and steel grinding balls. If you produce scrap metal in Uzbekistan, you are legally required to sell it to UZMK. The local sourcing satisfies ~80% of the company’s inputs and the remainder is purchased from international markets at a 70% higher price. Given that UZMK is the only buyer, they set the price of the local scrap supply.

The domestic market consumes all of the company’s production as the Uzbek economy grows rapidly and construction in Tashkent continues to boom. Oddly, the company sells to the private market via the Commodities Exchange, but all government sales are done in direct contracts. Again, this is an unfortunate example of the government not following its own rules and initiatives.

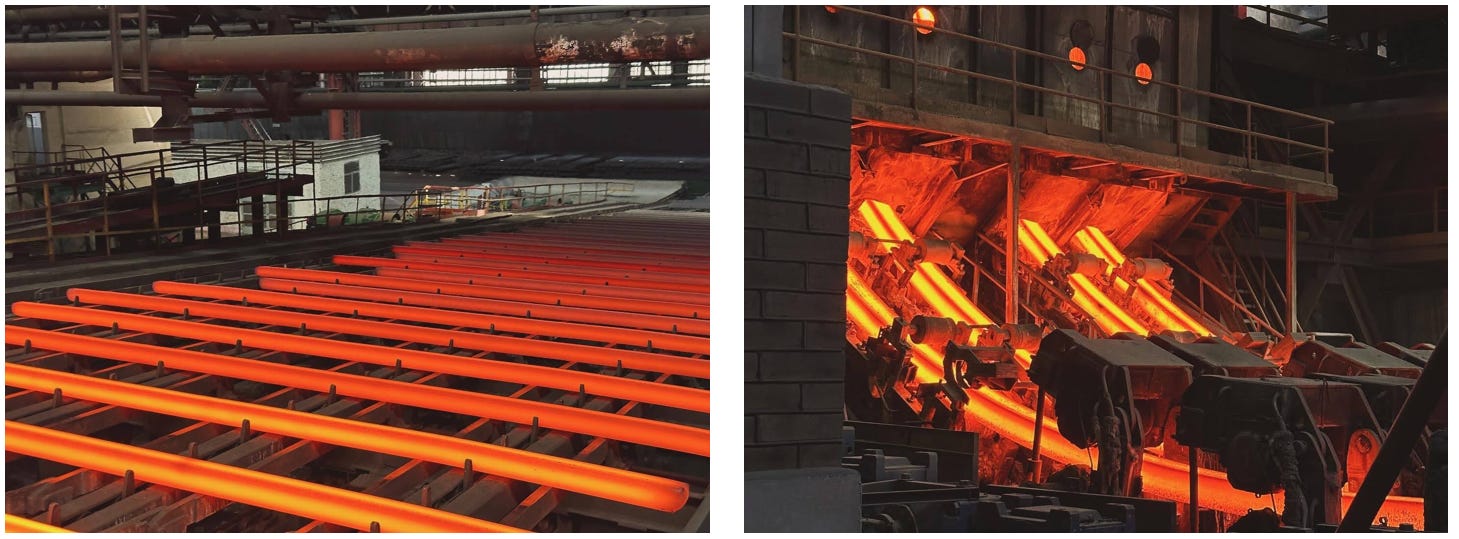

Nestled into the foothills on the Tajik / Uzbek border, the steel plant is a jaw-dropping example of Soviet-era industrialism. The main production building stretches 1.5 kilometers in length and towers over the landscape. The company employs a large portion of the surrounding community and has a dedicated power plant to run its three Bessember-style electric furnaces nonstop. We were lucky to tour the company’s facilities as they offer tours to the public - one just needs to make the 3 hour, very bumpy drive down from Tashkent.

As you enter the plant, you immediately notice the thick layer of iron dust covering every exposed surface. The company provides N95 masks to all tour participants as the iron dust easily gets inhaled into your lungs. The distant roar of the smelters reminds you of the rawness of this place. One cannot help but be reminded of Ayn Rand’s Rearden Steel as you descend down to the production floor. While much of the plant is automated, its age shows through with holes in the roof and the aging equipment. For the accountants, you can see and hear the accumulated depreciation of the property, plant, and equipment around you.

To be fair, this age is balanced by the brand-new facility being built as we speak on the same campus. The $800M project will double the plant’s capacity and will focus on the production of hot rolled coil products. The new facility originally had a completion goal of 2024 but judging by the current status of the construction, I assume this will be pushed back well into 2025. The construction of the plant is being managed by the international companies Danieli and Ronesans.

The company’s H1 2024 results are not great. Revenue shrunk ~4% in local currency and gross profits were down 13%. The company Operating income shrunk from $35M in H1 ‘23 to $29M in H2 ‘24, a ~20% decrease for the period. Net income shrunk 40% due to a smaller gain in FX and a massive jump in interest expenses. While long-term bank loans / debt decreased in the period, the company reported a 60% jump in short-term debt - it is unclear if this was an accounting adjustment moving long-term into short-term or if there was debt raised in the period that was due <1 year. The business’s leverage is nearing unsustainable levels. As Fitch points out in their February rating release, the company should hit peak leverage this year as the company’s debt load tops out and the new plant is yet to deliver accretive earnings.

My calculations put net debt to EBITDA leverage at ~4.9x for H1 run-rated results - this is 20% higher than its peer group of EM / FM industrial and metals businesses. However, these peers grew earnings by 10-12% in the last year, whereas UZMK’s earnings shrunk. It is important to note that more than 50% of the company’s debt is directly lent by the state or state-owned banks. While this is an unfortunate remnant of the Soviet era, the central control economic style, it is likely the government will support UZMK no matter what, given its importance to the economy and the quantum of borrowing from state banks. For all of the state-owned corporate ratings in Uzbekistan, Fitch actually includes the “state support” in their rating calculation.

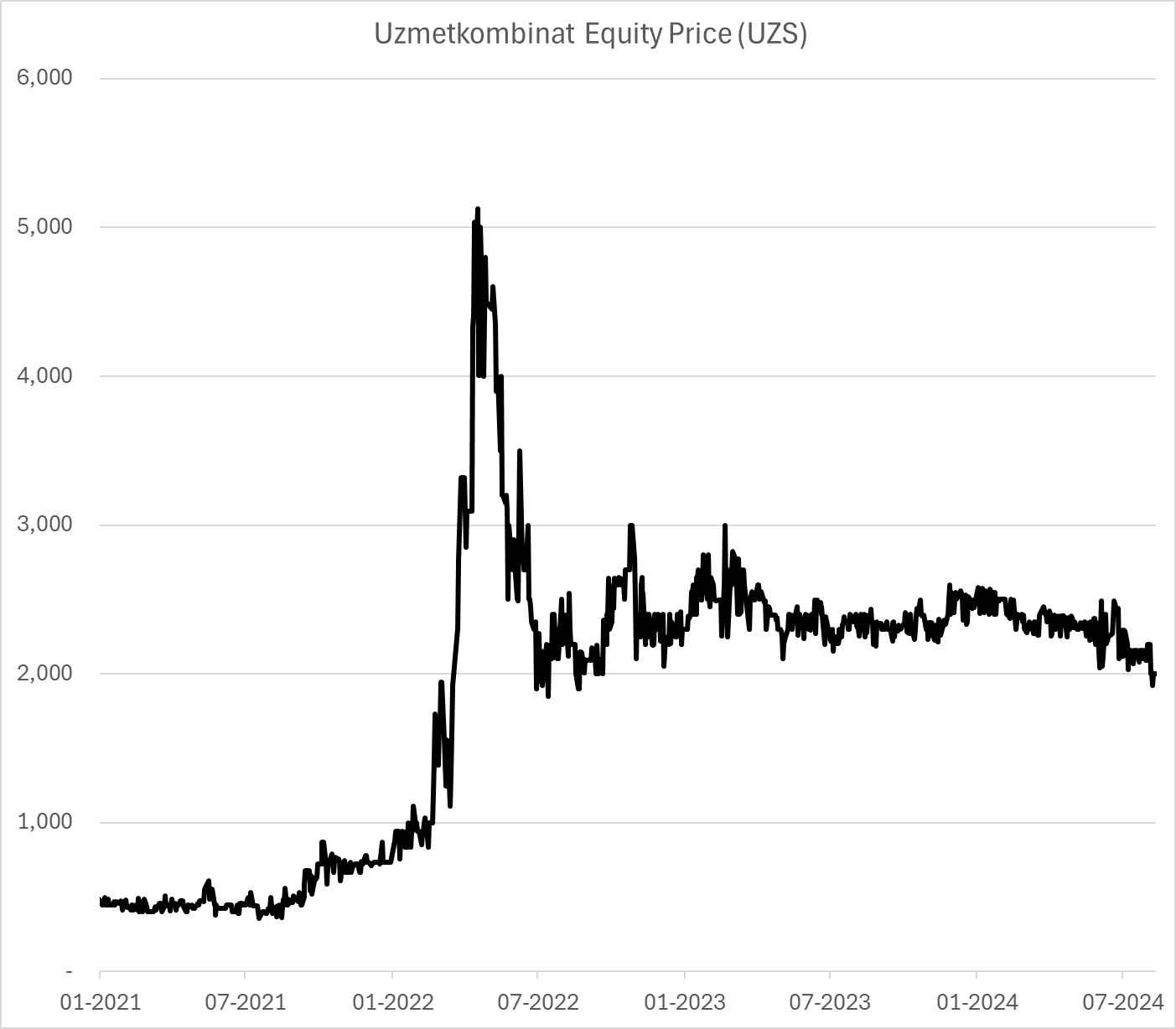

Uzmetkombinat’s stock has had a wild ride, to say the least - especially for a relatively sleepy business in the steel manufacturing industry. The company experienced a 10x increase in its share price from the beginning of 2021 to its peak in April 2022. The stock then lost 60% of its value in the span of 3 months and has now traded pretty flatly for the last 2 years.

The company currently trades at an LTM P/E of ~4.5x which compared to its peer group of frontier mining and metals companies is quite cheap to the 10-12x LTM earnings those companies are priced at. Some of this difference can be attributed to the lack of actual share float and foreign capital involvement in the stock itself. The stock only experiences ~$5,700 in monthly volume which is essentially nothing. To be fair. there is far more volume happening in the OTC market, but it is difficult to gather consolidated information on this market.

I think there is also a general market skepticism of the company’s management given its heavy State involvement and the understanding that the company will lose its monopoly position on all domestic scrap when more reforms are introduced. When this happens, the company's gross margin will likely nose dive due to the true price of scrap metal being priced into its production. The company reported in 2022 that local scrap trades at $185 / ton (again, this is a price the company itself sets as the only buyer allowed in the market) compared to imported scrap which is $385 / ton. Once the monopoly law is changed, the market should bring the local pricing up towards the regional price. For the sake of this argument, let’s assume local scrap goes from $185 / ton to just $250 as international buyers provide a new outlet for the country’s domestic scrap production - it would likely go even higher as international prices are all >$300. Assuming the company’s COGS is 60% attributable to input material (the average for industrial businesses), this would drive up the company’s COGS to ~110% of its revenue. In turn, this would force the company to raise prices significantly. It is unclear how much pricing power Uzmetkombinat possesses in the local market as more international suppliers from Russia, China, and India enter the growing market and UZMK is only satisfying 1/3rd of the domestic demand.

It will be interesting to see how the government reforms the market in the coming years and how UZMK will fit into these reforms. The company employs thousands of people - probably a large portion of the small town it is based in - and will need to make some hard decisions once the market opens up for competition and market-driven prices within their supply chain.

Uzbek Banks

As shared before, most of the equity value on the stock market is made up of the country’s many banks. In total, there are 33 commercial banks of which 12 are state-owned and control 70% ($35B) of the country’s banking assets. These state banks act as extensions of the government which are given subsidized funding and directed lending in order to pass credit onto various industries that the government deems to be needing capital. This is a Soviet artifact of the government where central command and directed lending is still quite standard. Unsurprisingly, as shown above with UZMK, much of this directed lending ends up in other SOEs leading to no actual credit extended into the private sector. When speaking to people within the banking market in Uzbekistan, many share that true NPLs of these banks are 15-25+% rather than the 2-8% many of them report. In normal circumstances, these banks would be insolvent and there would be a run for deposits by customers. Regulation is currently in the country’s legislator to bring the depository insurance down from complete coverage no matter the amount to $15,000 of coverage per account which would cover 99% of all deposit accounts in the country. I was curious to read the Deposit Guarantee Fund’s reports to see its liquidity position but the Fund has not published reports since 2022. The 2022 report shows $185M in fund assets which is in line with the coverage ratio of the FDIC and other deposit guarantee funds around the world in relation to their domestic banking deposits.

The largest private bank, Kapitalbank, is majority-owned by Uzbekistan’s most infamous oligarch, Alisher Usmanov through indirect companies. Usmanov’s Wikipedia page is worth reading. While he is clearly not a stand-up citizen by any account, he has led a wildly fascinating life by taking advantage of the chaos of the USSR dissolution, then owning massive mining assets, and parlaying that into being one of the more successful technology investors including pre-IPO investments into Facebook, Twitter, and Alibaba. He owns 3 yachts, some of the largest land holdings in Germany, and one of the largest private jets in the world - an Airbus A340 - which he named after his father.

If you are going to be an oligarch, at least be an interesting one like Usmanov, I guess.

Derek- This itself is enough to make me want to study his work a bit more: “While he is clearly not a stand-up citizen by any account, he has led a wildly fascinating life by taking advantage of the chaos of the USSR dissolution, then owning massive mining assets, and parlaying that into being one of the more successful technology investors including pre-IPO investments into Facebook, Twitter, and Alibaba.” I appreciate you sharing this. Thanks.

I just found your sub stack and I cannot stop reading. Thanks for providing free knowledge to the world